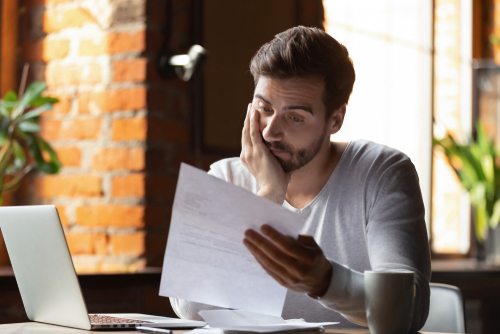

If the thought of paying off your student loan causes a bit of anxiety, worry no more. Here are some ways to pay it off faster. Check them out.

If the thought of paying off your student loan causes a bit of anxiety, worry no more. Here are some ways to pay it off faster. Check them out.

Sign Up for Auto-Pay

This might seem like the most obvious thing to do, and yet, some alums don’t take full advantage of it. The psychology of this works well. When you decide to put your payment on auto-draft, you never miss it. You get used to living on a certain amount of money. Better still, there are lenders who offer refinancing at lower rates, ranging from 1.8 percent to 7.84 percent. But there’s more: Some lenders offer cash-back bonuses. With that said, the catch is you give up important benefits like income-driven repayment and student loan forgiveness. However, refinancing can help you save a bunch – like thousands of dollars.

Pay Bi-Weekly

If you can swing this, it makes good sense. Why? Interest on your student loan accrues daily. Just cut your monthly payment in half and make two payments per month. This way, it might be easier to juggle your finances, as opposed to doling out one big chunk every month. Also, paying more often gives you the feeling that you’re making progress – and you are because of the daily accrual. #WinWin

Use the Debt Avalanche Method

With this approach, you’re paying off your highest interest debt first. Makes sense, right? After you do this, make minimum payments on all of your other loans. If you have any extra cash left over, pay your highest interest loan. Keep at this until you’re paid in full.

Claim the Student Loan Tax Deduction

This is cool. You can write off up to $2,500 of your student loan interest. Now, the amount you can write off depends on your income because there are phaseouts and gradual reductions in place. Just use the 1098-E form (you can get this from your loan servicer) to figure out how much interest you’ve paid. Then get going.

Pay While Still in School

Talk about getting a head start.You’ll cut down on interest (a good thing) while forgoing in-school deferment, and start paying down your debt pronto.

Pay Off Private Student Loans First

Should you have public and private student loans, this is the best strategy. Here’s why: private loans don’t offer student loan forgiveness or income-driven repayment. And they have limited deferment options. You’ll be better off doing this, given all the stipulations that exist for these kinds of loans.

Use Employer Repayment Assistance Programs

This is a sweet deal. Check with your employer to see if they offer such a program. Generally, they offer reimbursement or allocate funds to help you. Don’t forget to ask!

Pay During the Grace Period

This is the six-month period after graduation. While this might not be something that’s initially appealing, think it through. It helps keep interest in check and prevents your balance from growing during your grace period. Also, starting earlier means you’ll finish earlier. Gotta love that.

Consolidate Federal Student Loans

This is a great idea for those with limited resources. You can lower your payment and extend the repayment terms. You’ll most likely pay more interest, but for a short-time solution it’s a good one.

Exceed the Minimum Payment

If you have the means to make this happen, by all means, do it. Another great way to make incredible progress is to make double payments. If you can’t pay double, at least try to pay over the required amount. It’ll help eat away at the interest and eventually, the principal.

Student loans are great while you’re in school, right? They enable you to get the education you want. And while paying them off might be overwhelming, if you use these methods, you’ll be ahead of the game and pay them off sooner than you think.

Sources

107 Ways to Pay Off Student Loans Faster (That You Can Start Right Now)

Accounts payable (AP) is a crucial function to any business, as errors in the process put a company in problems. Although many businesses still use manual methods as they find the system to work fine, it requires a lot of precision from the accounts payable team. There are better – and more efficient – ways to manage AP through automation.

Accounts payable (AP) is a crucial function to any business, as errors in the process put a company in problems. Although many businesses still use manual methods as they find the system to work fine, it requires a lot of precision from the accounts payable team. There are better – and more efficient – ways to manage AP through automation. Increase of Public Debt Limit(S 1301) – This bill was enacted on Oct. 14 in order to increase the public debt limit. The debt was increased by $480 billion, the amount projected by the Treasury Department to be needed through early December in order to avoid surpassing the public debt limit. Had this stopgap legislation not been passed, it would have created the potential for a severe economic crisis in which the government would have run out of money to pay back existing debts, government salaries and other pre-existing obligations. The bill was initially introduced by Sen. Sherrod Brown (D-OH) on April 22; it passed in the House on Sept. 29 and in the Senate on Oct. 7. It was signed into law on Oct. 14.

Increase of Public Debt Limit(S 1301) – This bill was enacted on Oct. 14 in order to increase the public debt limit. The debt was increased by $480 billion, the amount projected by the Treasury Department to be needed through early December in order to avoid surpassing the public debt limit. Had this stopgap legislation not been passed, it would have created the potential for a severe economic crisis in which the government would have run out of money to pay back existing debts, government salaries and other pre-existing obligations. The bill was initially introduced by Sen. Sherrod Brown (D-OH) on April 22; it passed in the House on Sept. 29 and in the Senate on Oct. 7. It was signed into law on Oct. 14. The House recently released a nearly 900-page proposed bill that would make major changes to current tax laws. The bill is intended in large part to help pay for both the Biden Administration’s budget and infrastructure stimulus bill.

The House recently released a nearly 900-page proposed bill that would make major changes to current tax laws. The bill is intended in large part to help pay for both the Biden Administration’s budget and infrastructure stimulus bill. Based upon a recent McKinsey Global Survey, nearly 9 in 10 (87 percent) of management and above level respondents affirmed they are currently, or within the upcoming five years, dealing with the skill gap among their employees. With the vast majority of businesses experiencing or forecasting a skills-gap, how can they close or reduce this challenge?

Based upon a recent McKinsey Global Survey, nearly 9 in 10 (87 percent) of management and above level respondents affirmed they are currently, or within the upcoming five years, dealing with the skill gap among their employees. With the vast majority of businesses experiencing or forecasting a skills-gap, how can they close or reduce this challenge? According to the Sept. 8, 2021, release of the Federal Reserve’s Beige Book, the U.S. economy is facing many headwinds.

According to the Sept. 8, 2021, release of the Federal Reserve’s Beige Book, the U.S. economy is facing many headwinds. Today, 70 percent of college students graduate with an average of $30,000 in student loan debt. The average payment is nearly $400 a month and will take about 20 years to pay off. On an individual level, paying off high debt can delay hopes of saving to buy a house, start a family, launch a business or invest for retirement.

Today, 70 percent of college students graduate with an average of $30,000 in student loan debt. The average payment is nearly $400 a month and will take about 20 years to pay off. On an individual level, paying off high debt can delay hopes of saving to buy a house, start a family, launch a business or invest for retirement. So you want to save for a down payment for your dream house, but you aren’t sure how to get there. It might even feel overwhelming. But take heart, here are some tried and true methods that you can start today that will help you save sooner than you think.

So you want to save for a down payment for your dream house, but you aren’t sure how to get there. It might even feel overwhelming. But take heart, here are some tried and true methods that you can start today that will help you save sooner than you think. Choosing to implement new technology for your accounting needs is a big step toward improving your business. Accounting technology helps streamline the accounting system, thereby offering various benefits. However, poor implementation can impact your business negatively. To make your implementation a success, there are several mistakes that you must avoid.

Choosing to implement new technology for your accounting needs is a big step toward improving your business. Accounting technology helps streamline the accounting system, thereby offering various benefits. However, poor implementation can impact your business negatively. To make your implementation a success, there are several mistakes that you must avoid. Congressional Budget Justification Transparency Act of 2021 (S 272) – This bill mandates that federal agencies must make budget justification materials publicly available online. The Office of Management and Budget will be required to publish details regarding the agencies that submit budget justification materials to Congress and dates the materials are posted online, along with links to the materials. The bill was introduced by Sen. Gary Peters (D-MI) on Feb. 8, passed in the Senate and the House on Aug. 23 and is awaiting enactment by the president.

Congressional Budget Justification Transparency Act of 2021 (S 272) – This bill mandates that federal agencies must make budget justification materials publicly available online. The Office of Management and Budget will be required to publish details regarding the agencies that submit budget justification materials to Congress and dates the materials are posted online, along with links to the materials. The bill was introduced by Sen. Gary Peters (D-MI) on Feb. 8, passed in the Senate and the House on Aug. 23 and is awaiting enactment by the president.